Home

Uncategories

Insurance Expense T Account - What Are T Accounts Definition And Example - Adjusting entries occur at the end of the accounting period and affect one balance sheet account (an accrued liability) and one income statement account (an expense).

Insurance Expense T Account - What Are T Accounts Definition And Example - Adjusting entries occur at the end of the accounting period and affect one balance sheet account (an accrued liability) and one income statement account (an expense).

Insurance Expense T Account - What Are T Accounts Definition And Example - Adjusting entries occur at the end of the accounting period and affect one balance sheet account (an accrued liability) and one income statement account (an expense).. At the end of the accounting period (sep 30th, t account after aje), what is the net balance of costumes account? (a) in the t accounts, record the following transactions of potter pool services for june, identifying each entry by number: Don't claim the expense on this year's return. Set up t accounts for cash; Insurance expense is the amount that a company pays to get an insurance contract and any additional premium payments.

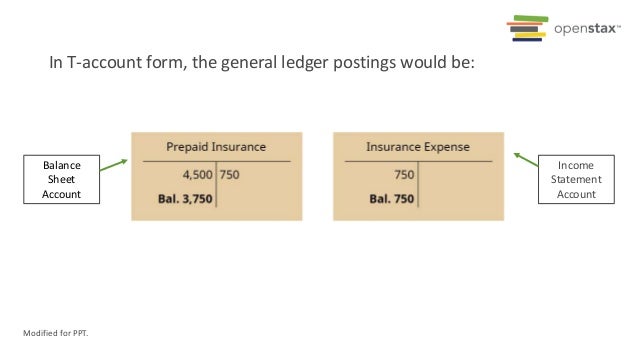

This is because that's what it has been set up. As the benefits of the expenses are recognized, the related asset account is decreased and expensed. The following steps have already been done for you: When the asset is charged to expense, the journal entry is to debit the insurance expense account and credit the prepaid insurance account. The payment made by the company is listed as an expense for the accounting period.

5 1 The Need For Adjusting Entries Financial Accounting from open.lib.umn.edu By account, we mean a summary record of all transactions relating to a particular item in a business. The following steps have already been done for you: This is because that's what it has been set up. The four basic steps in the closing process are: In accounting we open an account for each item in our records. The insurance provider charges an annual fee, called a premium, which will cover the business for 12 months. Only the expired portion of the premium should be presented as insurance expense. 31 bal. t accounts for wages payable, depreciation expense, laundry supplies expense, and insurance expense have been added below.

In accounting we open an account for each item in our records.

An entity initially records this expenditure as a prepaid expense (an asset), and then charges it to expense over the usage period. In the other liability and asset account section, there isn't a way to choose the expense. The costs that have expired should be reported in income statement accounts such as insurance expense, fringe benefits expense, etc. The expense, which is unexpired and is prepaid, is reported in the books of accounts under current assets. When the asset is charged to expense, the journal entry is to debit the insurance expense account and credit the prepaid insurance account. Insurance expense is the amount that a company pays to get an insurance contract and any additional premium payments. An example of a prepaid expense is insurance, which is frequently paid in advance for multiple future periods; The common type of expenses included in the financial statements of a business are employee salaries, depreciation, interest on a loan, rent, utility expenses, marketing cost, insurance cost for research and development, and other operating expenses. Insurance expense insurance expense is a charge a business incurs to protect its operations against adverse commercial or life events. Unexpired insurance premiums are reported as prepaid insurance (an asset account). You accrue expenses by recording an adjusting entry to the general ledger. Expired insurance premiums are reported as insurance expense. This is because that's what it has been set up.

Another item commonly found in the prepaid expenses account is prepaid rent. You can't include medical expenses that were paid by insurance companies or other sources. As a policyholder, the organization can select coverage for a vast array of events. If your employees pay a portion of the cost of their health insurance premium, you normally deduct the employee's share from his payroll check and record those payroll deductions in your accounting general ledger. Debit the appropriate expense account, and credit the appropriate.

Chapter 4 The Adjustment Process from image.slidesharecdn.com Set up t accounts for cash; The company signs a contract with an insurance company and agrees to pay periodic premiums in return for risk protection. You can't include medical expenses that were paid by insurance companies or other sources. Insurance expense is part of operating expenses in the income statement. Expenses lower owner's equity, but they are used to earn revenue. I've also added these articles for more information about payroll deductions: An example of a prepaid expense is insurance, which is frequently paid in advance for multiple future periods; Adjusting entries occur at the end of the accounting period and affect one balance sheet account (an accrued liability) and one income statement account (an expense).

You accrue expenses by recording an adjusting entry to the general ledger.

Debit the appropriate expense account, and credit the appropriate. An insurance expense occurs after a small business signs up with an insurance provider to receive protection cover. Make the appropriate adjusting entry. 31 bal. t accounts for wages payable, depreciation expense, laundry supplies expense, and insurance expense have been added below. The following steps have already been done for you: Closing the revenue accounts —transferring the credit balances in the revenue accounts to a clearing account called income summary. An insurance premium is an amount that an organization pays on behalf of its employees and other policies that the business has rendered to. Definition of insurance expense under the accrual basis of accounting, insurance expense is the cost of insurance that has been incurred, has expired, or has been used up during the current accounting period for the nonmanufacturing functions of a business. Each account balance listed in the unadjusted trial balance has been entered into its t account below, with the identification aug. The adjusting entry should be made as follows: The amount paid to acquire a specific coverage is known as premium. When viewed as an asset, the quality of insurance becomes the focal point. Insurance expense insurance expense is a charge a business incurs to protect its operations against adverse commercial or life events.

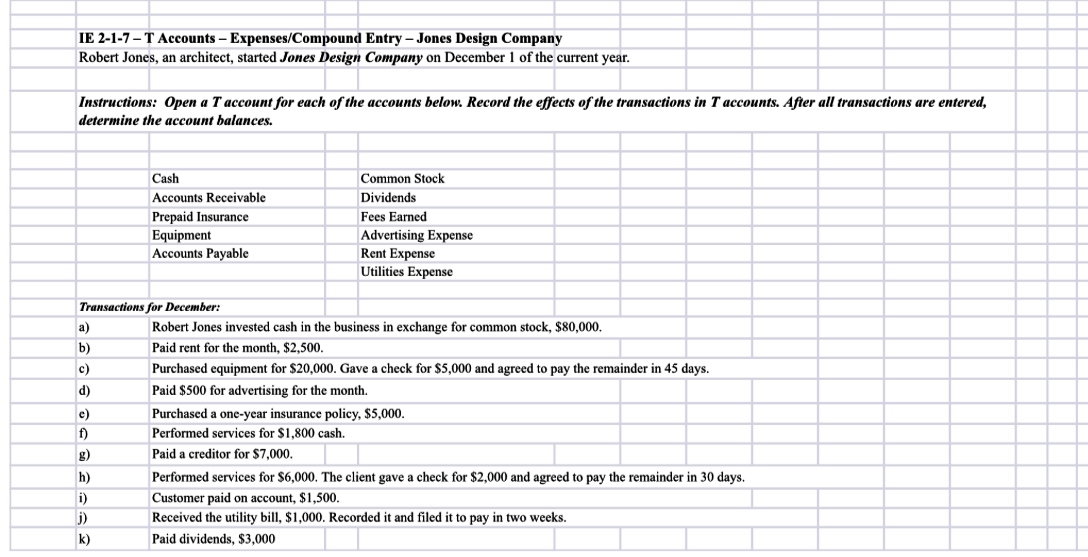

An entity initially records this expenditure as a prepaid expense (an asset), and then charges it to expense over the usage period. In accounting we open an account for each item in our records. Insurance expense insurance expense is a charge a business incurs to protect its operations against adverse commercial or life events. Generally, a claim for refund must be filed within 3 years from the date the original return was filed or within 2 years from the time the tax was paid, whichever is later. (a) in the t accounts, record the following transactions of potter pool services for june, identifying each entry by number:

Answered Instructions Open A T Account For Each Bartleby from prod-qna-question-images.s3.amazonaws.com When the asset is charged to expense, the journal entry is to debit the insurance expense account and credit the prepaid insurance account. (a) in the t accounts, record the following transactions of potter pool services for june, identifying each entry by number: The adjusting entry should be made as follows: 31 bal. t accounts for wages payable, depreciation expense, laundry supplies expense, insurance expense, and income summary have been added below. Don't claim the expense on this year's return. The following steps have already been done for you: Generally, a claim for refund must be filed within 3 years from the date the original return was filed or within 2 years from the time the tax was paid, whichever is later. Insurance expense is part of operating expenses in the income statement.

The common type of expenses included in the financial statements of a business are employee salaries, depreciation, interest on a loan, rent, utility expenses, marketing cost, insurance cost for research and development, and other operating expenses.

The company signs a contract with an insurance company and agrees to pay periodic premiums in return for risk protection. For the revenue accounts, debit entries. As you can see, the conventional account has the format of the letter t; Truck expense 55.insurance expense 56.miscellaneous expense 2. At the end of the accounting period (sep 30th, t account after aje), what is the net balance of costumes account? Accounts receivable 18,120 prepaid insurance 980 expenses automobile 20,650 salary expense 14,380 furniture and equipment 5,963 rent expense 10,320 liabilities automobile expense 859 accounts payable 1,590 utilities expense 1,213 owner's equity supplies expense 840 The common type of expenses included in the financial statements of a business are employee salaries, depreciation, interest on a loan, rent, utility expenses, marketing cost, insurance cost for research and development, and other operating expenses. Generally, a claim for refund must be filed within 3 years from the date the original return was filed or within 2 years from the time the tax was paid, whichever is later. An insurance expense occurs after a small business signs up with an insurance provider to receive protection cover. Join pro or pro plus and get lifetime access to our premium materials 31 bal. t accounts for wages payable, depreciation expense, laundry supplies expense, insurance expense, and income summary have been added below. The most common types of prepaid expenses are prepaid rent and prepaid insurance. The following steps have already been done for you:

0 Comments:

Post a Comment